If your business feels busy all the time but never quite under control, accounting is often where the problem hides. You have a lot to cover, including sales, marketing, customer service, and operations. And somewhere in the middle of all that circus sits accounting — quietly consuming time without ever feeling “done.”

This is how many small business owners end up working longer hours without actually moving the business forward..

Now, the problem with accounting is that it rarely looks like one big job. Instead, it appears as dozens of tiny, time-consuming tasks.

You enter a receipt here. Categorize an expense there. Then check a VAT entry. And then reconcile a bank transaction.

None of it seems dramatic. Until, suddenly, you find yourself deep in spreadsheets, simply because all those small accounting tasks added up. Not just in time, but in complexity, stress, and even money.

It happens to the best of us.

So, let’s talk about why those seemingly minor accounting tasks of financial admin become a massive drain on your business, and what you can do to prevent it.

There’s No Such Thing as a Quick Accounting Task

As a business owner, you’ve probably said this sentence at least once: “I’ll just quickly sort the accounts.”

But it wasn’t exactly quick, was it? And more importantly — it pulled you away from work that actually grows the business.

A typical small business owner like yourself deals with logging receipts, categorizing expenses, invoicing clients, following up on unpaid invoices, payroll processing, VAT tracking, financial reporting, tax preparation, and so on.

Individually, none of these is particularly scary, but collectively, they create a constant stream of admin work that keeps you operating the business — instead of actually leading it.

Just think of a simple task of uploading receipts. That upload turns into checking invoices, reconciling transactions, spotting duplicate entries, and figuring out why your bank balance and your bookkeeping software disagree. That’s why the biggest issue with accounting is that tasks are interconnected; one small entry can affect several other areas of your finances. For example:

Recording an expense affects profit reporting.

That profit reporting affects tax estimates.

Tax estimates then affect cash flow planning.

And cash flow planning affects your ability to invest or hire.

So, basically, that’s how small tasks accumulate over the course of a day. Even if you spend 10-15 minutes per day on accounting admin, that’s over 60 hours a year, or more than a week and a half of full-time work.

Now, besides being intertwined, accounting tasks are not purely administrative. In fact, they’re the foundation of your business. Every invoice recorded, expense categorized, and report generated gives a clearer picture of your business’s financial situation. No data point is insignificant, and together they create insights that guide your financial strategy and lead you to some of your biggest decisions.

Another reason accounting tasks pile up is simply growth.

Having more customers means more invoices, payments, expenses, and tax considerations. What used to take 10 minutes a week can suddenly take an hour. Or three. Or even half a day.

And by that point, accounting becomes something you avoid rather than something you manage. This is why, as your business grows, accounting stops being “just admin” and becomes a bottleneck — unless you build systems or hand it off.

The Mental Load

It’s fairly easy to understand that accounting takes time. But it’s not so obvious that it also takes your mental energy.

Financial tasks require concentration because mistakes have serious consequences. A misplaced decimal, a missing receipt, or incorrectly categorized expense can lead to complications later on, especially when it’s time to file taxes or review your finances.

It’s easy to overlook the mental load, but it does add up and can knock your productivity in the long run.

When Small Mistakes Ball up into Big Problems

As mentioned above, small accounting tasks matter because small errors compound quickly.

One incorrect entry can cause:

Incorrect profit calculations.

Inaccurate tax estimates.

Poor financial decisions.

Potential compliance issues.

And unlike many other business mistakes, accounting errors tend to appear at the worst possible moment. ? That’s why our advice is to stop treating accounting like a yearly obligation, as something you do purely because the government insists.

Accounting actually serves a much more valuable purpose, like helping you understand your business. Accurate financial data can answer questions like:

Which products/services are most profitable?

Where is money leaking out of the business?

Can I afford to hire someone new?

Is growth actually profitable?

Without reliable accounting, it’s hard to answer any of these questions properly and with confidence. And no one wants to play the financial roulette.

Why Outsourcing Accounting Makes Sense

At some point, you’ll realize that handling accounting internally simply isn’t the best use of your time.

You become aware of losing hours in the day, the mental load, the constant cross-checking, the stress of getting everything right. Plus, as you grow, the volume of transactions and reporting requirements becomes overwhelming.

At a certain point, staying involved in day-to-day accounting is no longer a strength — it becomes a bottleneck. Outsourcing is how owners step out of the weeds and back into decisions that actually move the business forward.

Underestimating Accounting Workload

Interestingly, many businesses underestimate accounting workload simply because they don’t track the time spent on it. If you measured it properly, the results might surprise you.

One simple way to understand this better is to actually track the time you spend on accounting tasks for a week or two. Some business owners use tools like Memtime to automatically capture time across applications, emails, documents, and meetings. This gives a much clearer picture of how much time is actually spent on tasks like reconciliation, reporting, and admin.

That’s how we know accounting tasks take much more time than originally anticipated.

To Conclude

Small accounting tasks don’t really look intimidating, but, like compound interest, their impact grows over time.

They can create so much stress and open your business to financial risks. But they also serve as the foundation for your smarter business decisions. It depends on how you approach and manage them.

The goal isn’t to manage accounting better. It’s to build a business where accounting no longer controls your time.

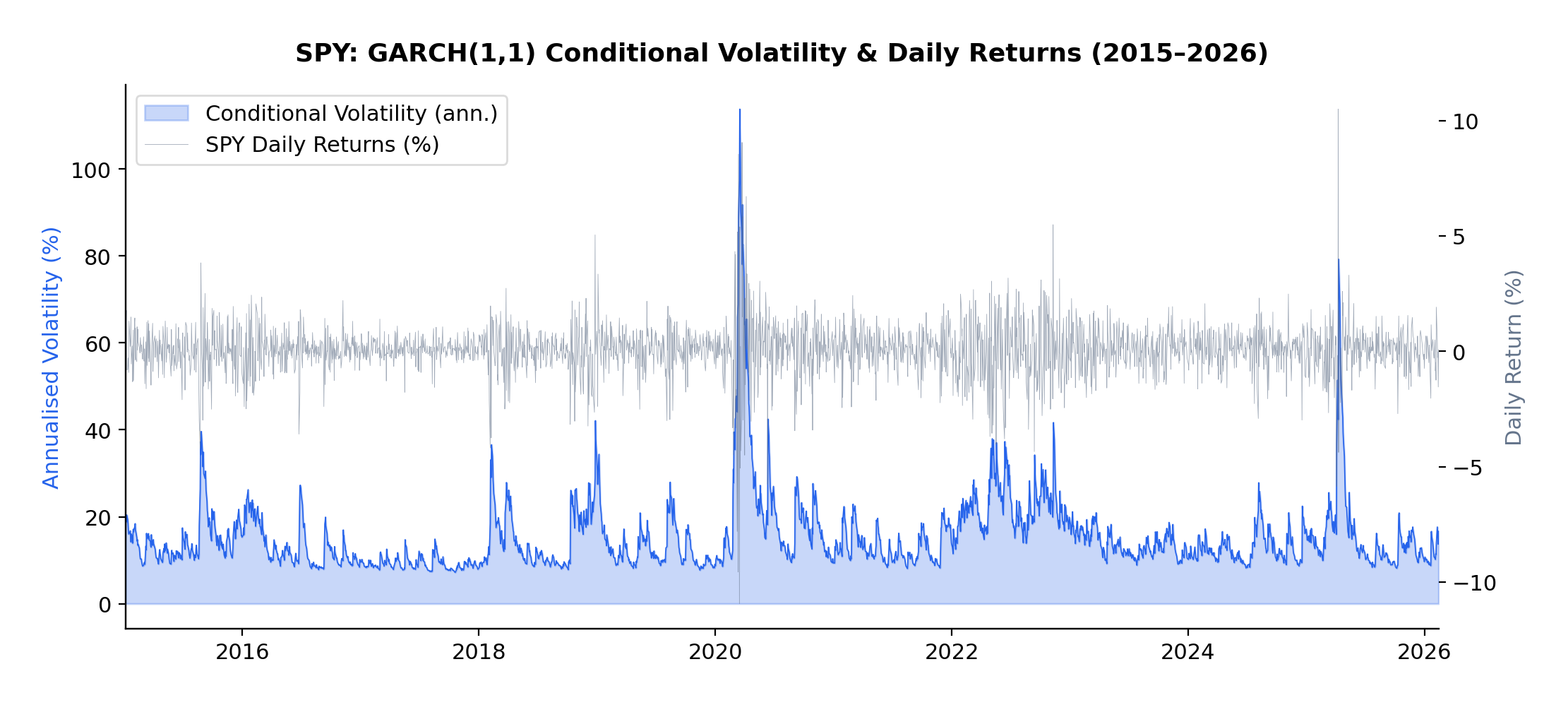

If you’ve been trading anything other than cash over the past eighteen months, you’ve noticed something peculiar: periods of calm tend to persist, but so do periods of chaos. A quiet Tuesday in January rarely suddenly explodes into volatility on Wednesday—market turbulence comes in clusters. This isn’t market inefficiency; it’s a fundamental stylized fact of financial markets, one that most quant models fail to properly account for.

The current volatility regime we’re navigating in early 2026 provides a perfect case study. Following the Federal Reserve’s policy pivot late in 2025, equity markets experienced a sharp correction, with the VIX spiking from around 15 to above 30 in a matter of weeks. But here’s what interests me as a researcher: that elevated volatility didn’t dissipate overnight. It lingered, exhibiting the characteristic “slow decay” that the GARCH framework was designed to capture.

In this article, I present an empirical analysis of volatility dynamics across five major asset classes—the S&P 500 (SPY), US Treasuries (TLT), Gold (GLD), Oil (USO), and Bitcoin (BTC-USD)—over the ten-year period from January 2015 to February 2026. Using both GARCH(1,1) and EGARCH(1,1,1) models, I characterize volatility persistence and leverage effects, revealing striking differences across asset classes that have direct implications for risk management and trading strategy design.

This extends my earlier work on VIX derivatives and correlation trading, where understanding the time-varying nature of volatility is essential for pricing complex derivatives and managing portfolio risk through volatile regimes.

Understanding Volatility Clustering

Before diving into the results, let’s build some intuition about what GARCH actually captures—and why it matters.

Volatility clustering refers to the empirical observation that large price changes tend to be followed by large price changes, and small changes tend to follow small changes. If the market experiences a turbulent day, don’t expect immediate tranquility the next day. Conversely, a period of quiet trading often continues uninterrupted.

This phenomenon was formally modeled by Robert Engle in his landmark 1982 paper, “Autoregressive Conditional Heteroskedasticity with Estimates of the Variance of United Kingdom Inflation,” which introduced the ARCH (Autoregressive Conditional Heteroskedasticity) model. Engle’s insight was revolutionary: rather than assuming constant variance (homoskedasticity), he modeled variance itself as a time-varying process that depends on past shocks.

Tim Bollerslev extended this work in 1986 with the GARCH (Generalized ARCH) model, which proved more parsimonious and flexible. Then, in 1991, Daniel Nelson introduced the EGARCH (Exponential GARCH) model, which could capture the asymmetric response of volatility to positive versus negative returns—the famous “leverage effect” where negative shocks tend to increase volatility more than positive shocks of equal magnitude.

The Mathematics

The standard GARCH(1,1) model specifies:

where:

σt2 is the conditional variance at time t

rt-12 is the squared return from the previous period (the “shock”)

σt-12 is the previous period’s conditional variance

α measures how quickly volatility responds to new shocks

β measures the persistence of volatility shocks

The sum α + β represents overall volatility persistence

The key parameter here is α + β. If this sum is close to 1 (as it typically is for financial assets), volatility shocks decay slowly—a phenomenon I observed firsthand during the 2025-2026 correction. We can calculate the “half-life” of a volatility shock as:

For example, with α + β = 0.97, a volatility shock takes approximately ln(0.5)/ln(0.97) ≈ 23 days to decay by half.

The EGARCH model modifies this framework to capture asymmetry:

The parameter γ (gamma) captures the leverage effect. A negative γ means that negative returns generate more volatility than positive returns of equal magnitude—which is precisely what we observe in equity markets and, as we’ll see, in Bitcoin.

For each asset in the sample, I computed daily log returns as:

The multiplication by 100 converts returns to percentage terms, which improves numerical convergence when estimating the models.

I then fitted two volatility models to each asset’s return series:

GARCH(1,1): The workhorse model that captures volatility clustering through the autoregressive structure of conditional variance

EGARCH(1,1,1): The exponential GARCH model that additionally captures leverage effects through the asymmetric term

All models were estimated using Python’s arch package with normally distributed innovations. The sample period spans January 2015 to February 2026, encompassing multiple distinct volatility regimes including:

The 2015-2016 oil price collapse

The 2018 Q4 correction

The COVID-19 volatility spike of March 2020

The 2022 rate-hike cycle

The 2025-2026 post-pivot correction

This rich variety of regimes makes the sample ideal for studying volatility dynamics across different market conditions.

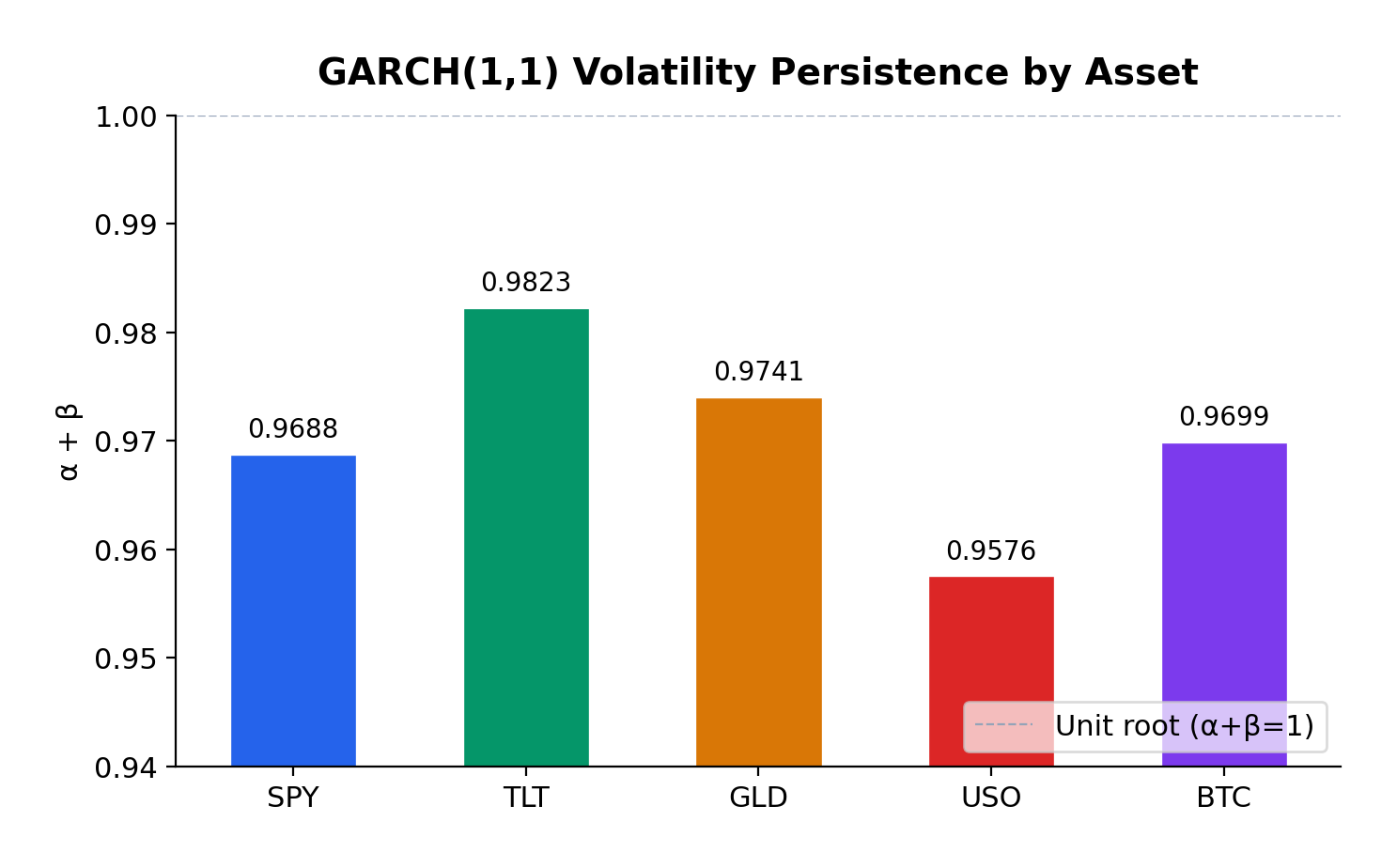

GARCH(1,1) Estimates

The GARCH(1,1) model reveals substantial variation in volatility dynamics across asset classes:

Asset

α (alpha)

β (beta)

Persistence (α+β)

Half-life (days)

AIC

S&P 500

0.1810

0.7878

0.9688

~23

7130.4

US Treasuries

0.0683

0.9140

0.9823

~38

7062.7

Gold

0.0631

0.9110

0.9741

~27

7171.9

Oil

0.1271

0.8305

0.9576

~16

11999.4

Bitcoin

0.1228

0.8470

0.9699

~24

20789.6

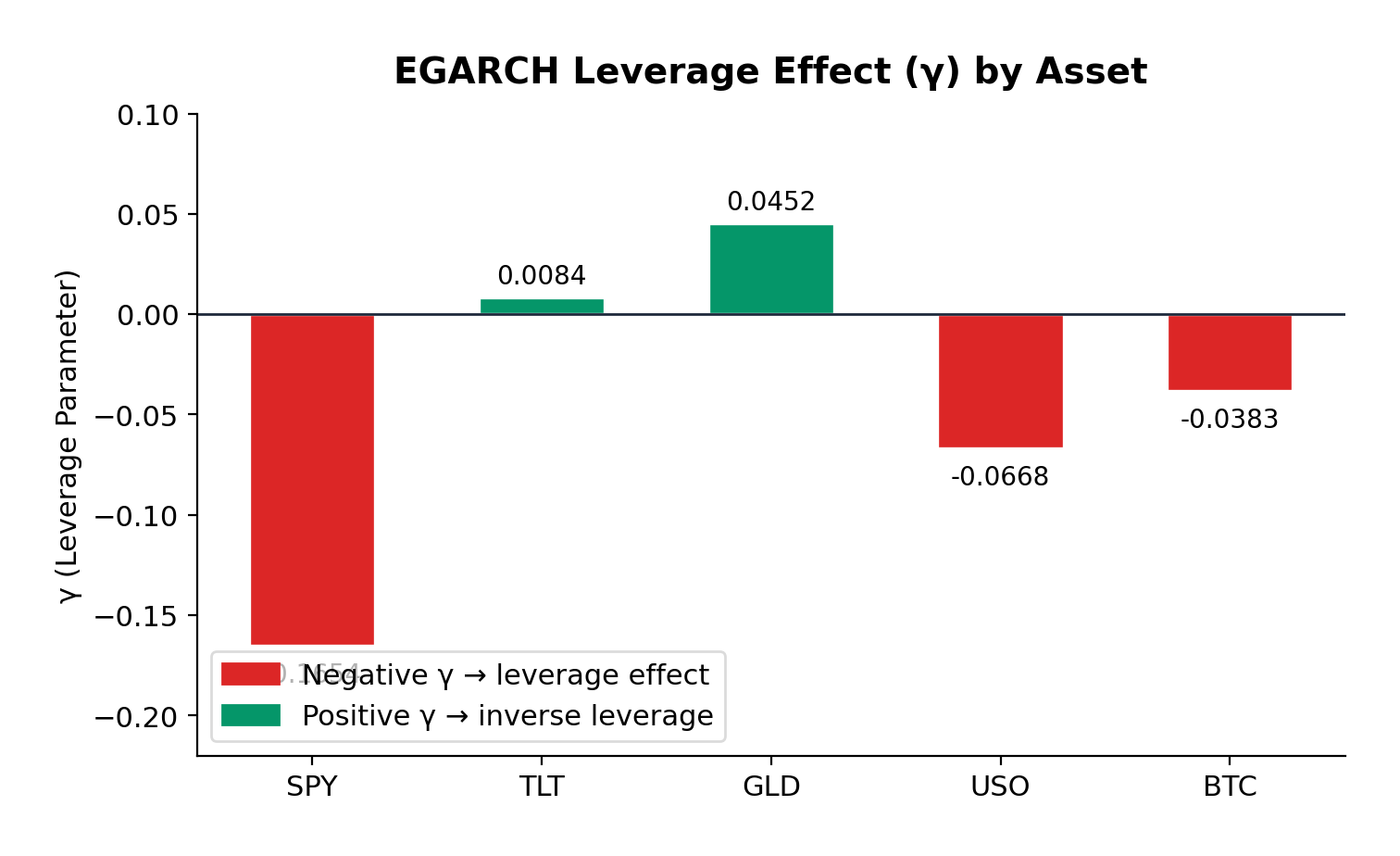

EGARCH(1,1,1) Estimates

The EGARCH model additionally captures leverage effects:

Asset

α (alpha)

β (beta)

γ (gamma)

Persistence

AIC

S&P 500

0.2398

0.9484

-0.1654

1.1882

7022.6

US Treasuries

0.1501

0.9806

0.0084

1.1307

7063.5

Gold

0.1205

0.9721

0.0452

1.0926

7146.9

Oil

0.2171

0.9564

-0.0668

1.1735

12002.8

Bitcoin

0.2505

0.9377

-0.0383

1.1882

20773.9

Volatility Persistence

All five assets exhibit high volatility persistence, with α + β ranging from 0.9576 (Oil) to 0.9823 (US Treasuries). These values are remarkably consistent with the classic empirical findings from Engle (1982) and Bollerslev (1986), who first documented this phenomenon in inflation and stock market data respectively.

US Treasuries show the highest persistence (0.9823), meaning volatility shocks in the bond market take longer to decay—approximately 38 days to half-life. This makes intuitive sense: Federal Reserve policy changes, which are the primary drivers of Treasury volatility, tend to have lasting effects that persist through subsequent meetings and economic data releases.

Gold exhibits the second-highest persistence (0.9741), consistent with its role as a long-term store of value. Macroeconomic uncertainties—geopolitical tensions, currency debasement fears, inflation scares—don’t resolve quickly, and neither does the associated volatility.

S&P 500 and Bitcoin show similar persistence (~0.97), with half-lives of approximately 23-24 days. This suggests that equity market volatility shocks, despite their reputation for sudden spikes, actually decay at a moderate pace.

Oil has the lowest persistence (0.9576), which makes sense given the more mean-reverting nature of commodity prices. Oil markets can experience rapid shifts in sentiment based on supply disruptions or demand changes, but these shocks tend to resolve more quickly than in financial assets.

Leverage Effects

The EGARCH γ parameter reveals asymmetric volatility responses—the leverage effect that Nelson (1991) formalized:

S&P 500 (γ = -0.1654): The strongest negative leverage effect in the sample. A 1% drop in equities increases volatility significantly more than a 1% rise. This is the classic equity pattern: bad news is “stickier” than good news. For options traders, this means that protective puts are more expensive than equivalent out-of-the-money calls during volatile periods—a direct consequence of this asymmetry.

Bitcoin (γ = -0.0383): Moderate negative leverage, weaker than equities but still significant. The cryptocurrency market shows asymmetric reactions to price movements, with downside moves generating more volatility than upside moves. This is somewhat surprising given Bitcoin’s retail-dominated nature, but consistent with the hypothesis that large institutional players are increasingly active in crypto markets.

Oil (γ = -0.0668): Moderate negative leverage, similar to Bitcoin. The energy market’s reaction to geopolitical events (which tend to be negative supply shocks) contributes to this asymmetry.

Gold (γ = +0.0452): Here’s where it gets interesting. Gold exhibits a slight positive gamma—the opposite of the equity pattern. Positive returns slightly increase volatility more than negative returns. This is consistent with gold’s safe-haven role: when risk assets sell off and investors flee to gold, the resulting price spike in gold can be accompanied by increased trading activity and volatility. Conversely, gradual gold price increases during calm markets occur with declining volatility.

US Treasuries (γ = +0.0084): Essentially symmetric. Treasury volatility doesn’t distinguish between positive and negative returns—which makes sense, since Treasuries are priced primarily on interest rate expectations rather than “good” or “bad” news in the equity sense.

Model Fit

The AIC (Akaike Information Criterion) comparison shows that EGARCH provides a materially better fit for the S&P 500 (7022.6 vs 7130.4) and Bitcoin (20773.9 vs 20789.6), where significant leverage effects are present. For Gold and Treasuries, GARCH performs comparably or slightly better, consistent with the absence of significant leverage asymmetry.

1. Volatility Forecasting and Position Sizing

The high persistence values across all assets have direct implications for position sizing during volatile regimes. If you’re trading options or managing a portfolio, the GARCH framework tells you that elevated volatility will likely persist for weeks, not days. This suggests:

Don’t reduce risk too quickly after a volatility spike. The half-life analysis shows that it takes 2-4 weeks for half of a volatility shock to dissipate. Cutting exposure immediately after a correction means you’re selling low vol into the spike.

Expect re-leveraging opportunities. Once vol peaks and begins decaying, there’s a window of several weeks where volatility is still elevated but declining—potentially favorable for selling vol (e.g., writing covered calls or selling volatility swaps).

2. Options Pricing

The leverage effects have material implications for option pricing:

Equity options (S&P 500) should price in significant skew—put options are relatively more expensive than calls. If you’re buying protection (e.g., buying SPY puts for portfolio hedge), you’re paying a premium for this asymmetry.

Bitcoin options show similar but weaker asymmetry. The market is still relatively young, and the vol surface may not fully price in the leverage effect—potentially an edge for sophisticated options traders.

Gold options exhibit the opposite pattern. Call options may be relatively cheaper than puts, reflecting gold’s tendency to experience vol spikes on rallies (as opposed to selloffs).

3. Portfolio Construction

For multi-asset portfolios, the differing persistence and leverage characteristics suggest tactical allocation shifts:

During risk-on regimes: Low persistence in oil suggests faster mean reversion—commodity exposure might be appropriate for shorter time horizons.

During risk-off regimes: High persistence in Treasuries means bond market volatility decays slowly. Duration hedges need to account for this extended volatility window.

Diversification benefits: The low correlation between equity and Treasury volatility dynamics supports the case for mixed-asset portfolios—but the high persistence in both suggests that when one asset class enters a high-vol regime, it likely persists for weeks.

4. Trading Volatility Directly

For traders who express views on volatility itself (VIX futures, variance swaps, volatility ETFs):

The persistence framework suggests that VIX spikes should be traded as mean-reverting (which they are), but with the expectation that complete normalization takes 30-60 days.

The leverage effect in equities means that vol strategies should be positioned for asymmetric payoffs—long vol positions benefit more from downside moves than equivalent upside moves.

At the bottom of the post is the complete Python code used to generate these results. The code uses yfinance for data download and the arch package for model estimation. It’s designed to be easily extensible—you can add additional assets, change the date range, or experiment with different GARCH variants (GARCH-M, TGARCH, GJR-GARCH) to capture different aspects of the volatility dynamics.

This analysis confirms that volatility clustering is a universal phenomenon across asset classes, but the specific characteristics vary meaningfully:

Volatility persistence is universally high (α + β ≈ 0.95–0.98), meaning volatility shocks take weeks to months to decay. This has important implications for position sizing and risk management.

Leverage effects vary dramatically across asset classes. Equities show strong negative leverage (bad news increases vol more than good news), while gold shows slight positive leverage (opposite pattern), and Treasuries show no meaningful asymmetry.

The half-life of volatility shocks ranges from approximately 16 days (oil) to 38 days (Treasuries), providing a quantitative guide for expected duration of volatile regimes.

These findings extend naturally to my ongoing work on volatility derivatives and correlation trading. Understanding the persistence and asymmetry of volatility is essential for pricing VIX options, variance swaps, and other vol-sensitive products—as well as for managing the tail risk that inevitably accompanies high-volatility regimes like the one we’re navigating in early 2026.

References

Engle, R.F. (1982). “Autoregressive Conditional Heteroskedasticity with Estimates of the Variance of United Kingdom Inflation.” Econometrica, 50(4), 987-1007.

Bollerslev, T. (1986). “Generalized Autoregressive Conditional Heteroskedasticity.” Journal of Econometrics, 31(3), 307-327.

Nelson, D.B. (1991). “Conditional Heteroskedasticity in Asset Returns: A New Approach.” Econometrica, 59(2), 347-370.

All models estimated using Python’s arch package with normal innovations. Data source: Yahoo Finance. The analysis covers the period January 2015 through February 2026, comprising approximately 2,800 trading days.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.