Google I/O 2026 starts on May 19, and while we already have a pretty good idea of what to expect, there’s plenty of room for surprises. The tech giant has been all-in on AI for the past few years, and that probably won’t change, but there could be a few hardware announcements on tap this year.

From Android XR glasses to hearing more about Aluminum OS, there’s a lot to look forward to. Below, we’ll fill you in on what we expect Google to talk about during the I/O keynote.

More AI features

We expect Google to announce several new artificial intelligence features that integrate further into its products. Now that agentic AI is all the rage, we’ll most likely see Google lean even further in this direction. This type of AI can perform tasks on your behalf, like controlling your computer, with minimal oversight. We’ll have to wait and see what and how many AI features Google announces this time.

Let’s also not exclude updates to existing or new products that Google could announce. Veo, Lyria, Beam and countless others could get some spotlight at this year’s conference.

Veo and Lyria are Google’s AI-generated video and music tools, respectively, and have continued to improve since they were originally announced. Beam is an ambitious and futuristic way of video conferencing that uses several cameras to make you appear as though you’re speaking directly to the person in front of you as a 3D model.

Gemini 4.0

The next generation Gemini is likely going to be announced at Google I/O 2026

Thomas Fuller/Getty Images

Among all the AI announcements, we’re expecting Google to spend a significant amount of time talking about its flagship AI model for Gemini. Whether it gets a solid 4.0 status or something like a 3.8, we know the new version of Gemini will likely be one of the biggest announcements of Google I/O 2026.

Exactly what Google has been working on with Gemini is anyone’s guess. It’s easy enough to assume that the latest model will be smarter and faster than previous models, but Gemini itself is in nearly every Google product these days, so how the latest and greatest AI from Google trickles down will be interesting to see.

Google recently released a new notebooks feature for Gemini that will let you store sources for a particular topic in one place for easy access. Notebooks are self-contained databases full of sources on a particular topic that you can continue to add to. Gemini will use a notebook for context, so you don’t have to start all over again with information sources.

Those notebooks also sync directly with Google’s AI research assistant NotebookLM, allowing you to create a host of different outputs, like video overviews, charts and more. One of the main differentiators between NotebookLM and Gemini is that NotebookLM will only use your notebook as the source of truth, whereas Gemini will scour the internet with the notebook’s context for the search.

Gemini can also now create dynamic and interactive simulations directly in your chats when you ask it to “show you” or “visualize” something.

Google hasn’t slowed its rollout of Gemini features, so a lot more are likely on their way with the latest version of the AI model.

Android XR Glasses

Android XR will most certainly steal some of the spotlight during this year’s I/O conference.

Andrew Lanxon/CNET

Google showed off its Android XR glasses at last year’s I/O, along with a few partnerships it formed to create them, so we’ll likely see the smart glasses become more of a product than a concept this year.

Smart glasses are gaining popularity, and Google took awhile getting back into the space after its first swing in the sector. Google Glass was way ahead of its time, but from the demos we’ve seen of Android XR, that patience may have paid off.

Google’s first set of “smart glasses” back in 2013 was an obvious pair of spectacles with a protruding lens that the wearer could view information on, and even take photos and record video. The product was met with immediate and significant pushback as an invasion of privacy, as well as being elitist and rude. This eventually resulted in the term for the wearers as “Glassholes.”

A lot has changed since the introduction of Google Glass, and Android XR glasses won’t look nearly as obvious when released, which could make it even creepier, but at least they’ll come with a load of usable features like heads-up notifications, live translation and Gemini Live. They’re also launching into an established market now, with smart glasses competitors from Meta’s collaborations with Ray-Ban, Oakley and more. Samsung’s own Galaxy XR headset runs on the Android XR platform and is already available to purchase. This first piece of hardware running on the platform paves the way for more hardware, with smart glasses being a natural next step.

Google I/O could bring us more demos, final hardware details and a release date for when you’ll be able to get Android XR glasses in your hands. Given that there are multiple partners in the ring, the price ranges could vary, potentially offering both entry-level and high-end offerings.

Android 17

Google/Screenshot by CNET

Android is Google’s playground for showcasing the best of its AI features, though some of them may be exclusive to the new Pixel phones we expect to see later this year.

Google released the first beta version of Android 17, its phone-operating system, back in February, and three additional betas have been released since, with the latest in mid-April. We can expect the latest version of the OS to be released in its final form sometime in June or July, shortly before we expect the next family of Pixel devices to be announced. For the past few years, the new Pixel lineup has been announced in August during the Made by Google event.

So far, there are no blockbuster features in the Android 17 beta, but Google has introduced interesting tweaks throughout. One of the most interesting features so far is app bubbles, which allows you to quickly access any app in a floating window and dismiss it to a bubble on your screen.

Last year, Google separated its Android announcements into a separate show a week before its I/O conference: The Android Show. This allowed Google to spend more time talking about AI without sacrificing the announcements it had on tap for Android. Whether The Android Show will return this year remains to be seen — though reportedly, a YouTube placeholder for the event was accidentally set live last week before being taken down.

Aluminum OS

One of the most interesting projects Google has been cooking up is a new operating system that merges Android and ChromeOS. Dubbed Aluminum OS, the product will bring Android to laptops and other devices with the full Chrome web browsing experience.

When exactly we’ll see hardware for the new OS is still unknown, but Google could surprise us with partnership announcements or even a full product announcement at I/O this year. The return of a Google-made Pixelbook doesn’t seem out of the realm of possibility, either.

Merging both of Google’s operating systems will likely bring a more seamless software experience between how AluminumOS computers and Android phones interact.

If you’ve been trading anything other than cash over the past eighteen months, you’ve noticed something peculiar: periods of calm tend to persist, but so do periods of chaos. A quiet Tuesday in January rarely suddenly explodes into volatility on Wednesday—market turbulence comes in clusters. This isn’t market inefficiency; it’s a fundamental stylized fact of financial markets, one that most quant models fail to properly account for.

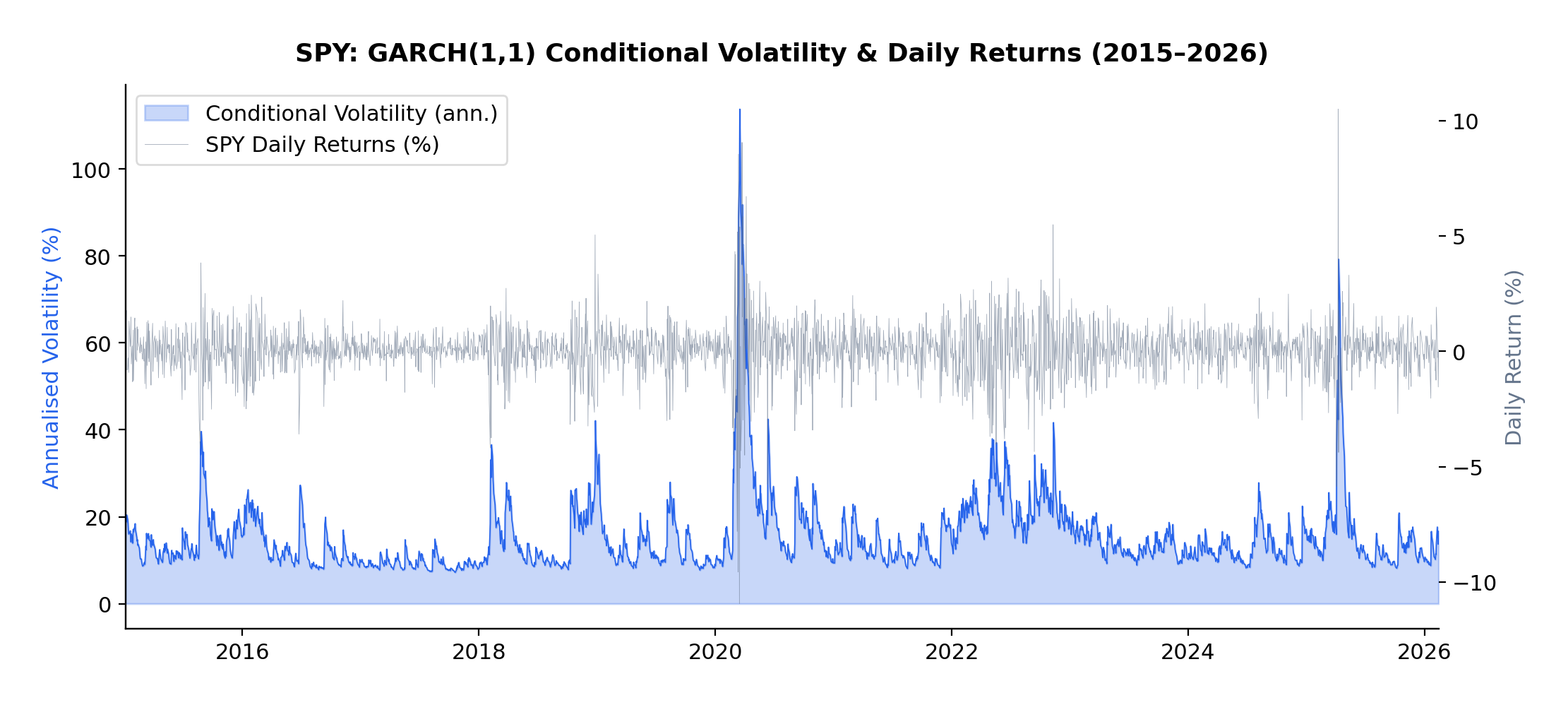

The current volatility regime we’re navigating in early 2026 provides a perfect case study. Following the Federal Reserve’s policy pivot late in 2025, equity markets experienced a sharp correction, with the VIX spiking from around 15 to above 30 in a matter of weeks. But here’s what interests me as a researcher: that elevated volatility didn’t dissipate overnight. It lingered, exhibiting the characteristic “slow decay” that the GARCH framework was designed to capture.

In this article, I present an empirical analysis of volatility dynamics across five major asset classes—the S&P 500 (SPY), US Treasuries (TLT), Gold (GLD), Oil (USO), and Bitcoin (BTC-USD)—over the ten-year period from January 2015 to February 2026. Using both GARCH(1,1) and EGARCH(1,1,1) models, I characterize volatility persistence and leverage effects, revealing striking differences across asset classes that have direct implications for risk management and trading strategy design.

This extends my earlier work on VIX derivatives and correlation trading, where understanding the time-varying nature of volatility is essential for pricing complex derivatives and managing portfolio risk through volatile regimes.

Understanding Volatility Clustering

Before diving into the results, let’s build some intuition about what GARCH actually captures—and why it matters.

Volatility clustering refers to the empirical observation that large price changes tend to be followed by large price changes, and small changes tend to follow small changes. If the market experiences a turbulent day, don’t expect immediate tranquility the next day. Conversely, a period of quiet trading often continues uninterrupted.

This phenomenon was formally modeled by Robert Engle in his landmark 1982 paper, “Autoregressive Conditional Heteroskedasticity with Estimates of the Variance of United Kingdom Inflation,” which introduced the ARCH (Autoregressive Conditional Heteroskedasticity) model. Engle’s insight was revolutionary: rather than assuming constant variance (homoskedasticity), he modeled variance itself as a time-varying process that depends on past shocks.

Tim Bollerslev extended this work in 1986 with the GARCH (Generalized ARCH) model, which proved more parsimonious and flexible. Then, in 1991, Daniel Nelson introduced the EGARCH (Exponential GARCH) model, which could capture the asymmetric response of volatility to positive versus negative returns—the famous “leverage effect” where negative shocks tend to increase volatility more than positive shocks of equal magnitude.

The Mathematics

The standard GARCH(1,1) model specifies:

where:

σt2 is the conditional variance at time t

rt-12 is the squared return from the previous period (the “shock”)

σt-12 is the previous period’s conditional variance

α measures how quickly volatility responds to new shocks

β measures the persistence of volatility shocks

The sum α + β represents overall volatility persistence

The key parameter here is α + β. If this sum is close to 1 (as it typically is for financial assets), volatility shocks decay slowly—a phenomenon I observed firsthand during the 2025-2026 correction. We can calculate the “half-life” of a volatility shock as:

For example, with α + β = 0.97, a volatility shock takes approximately ln(0.5)/ln(0.97) ≈ 23 days to decay by half.

The EGARCH model modifies this framework to capture asymmetry:

The parameter γ (gamma) captures the leverage effect. A negative γ means that negative returns generate more volatility than positive returns of equal magnitude—which is precisely what we observe in equity markets and, as we’ll see, in Bitcoin.

For each asset in the sample, I computed daily log returns as:

The multiplication by 100 converts returns to percentage terms, which improves numerical convergence when estimating the models.

I then fitted two volatility models to each asset’s return series:

GARCH(1,1): The workhorse model that captures volatility clustering through the autoregressive structure of conditional variance

EGARCH(1,1,1): The exponential GARCH model that additionally captures leverage effects through the asymmetric term

All models were estimated using Python’s arch package with normally distributed innovations. The sample period spans January 2015 to February 2026, encompassing multiple distinct volatility regimes including:

The 2015-2016 oil price collapse

The 2018 Q4 correction

The COVID-19 volatility spike of March 2020

The 2022 rate-hike cycle

The 2025-2026 post-pivot correction

This rich variety of regimes makes the sample ideal for studying volatility dynamics across different market conditions.

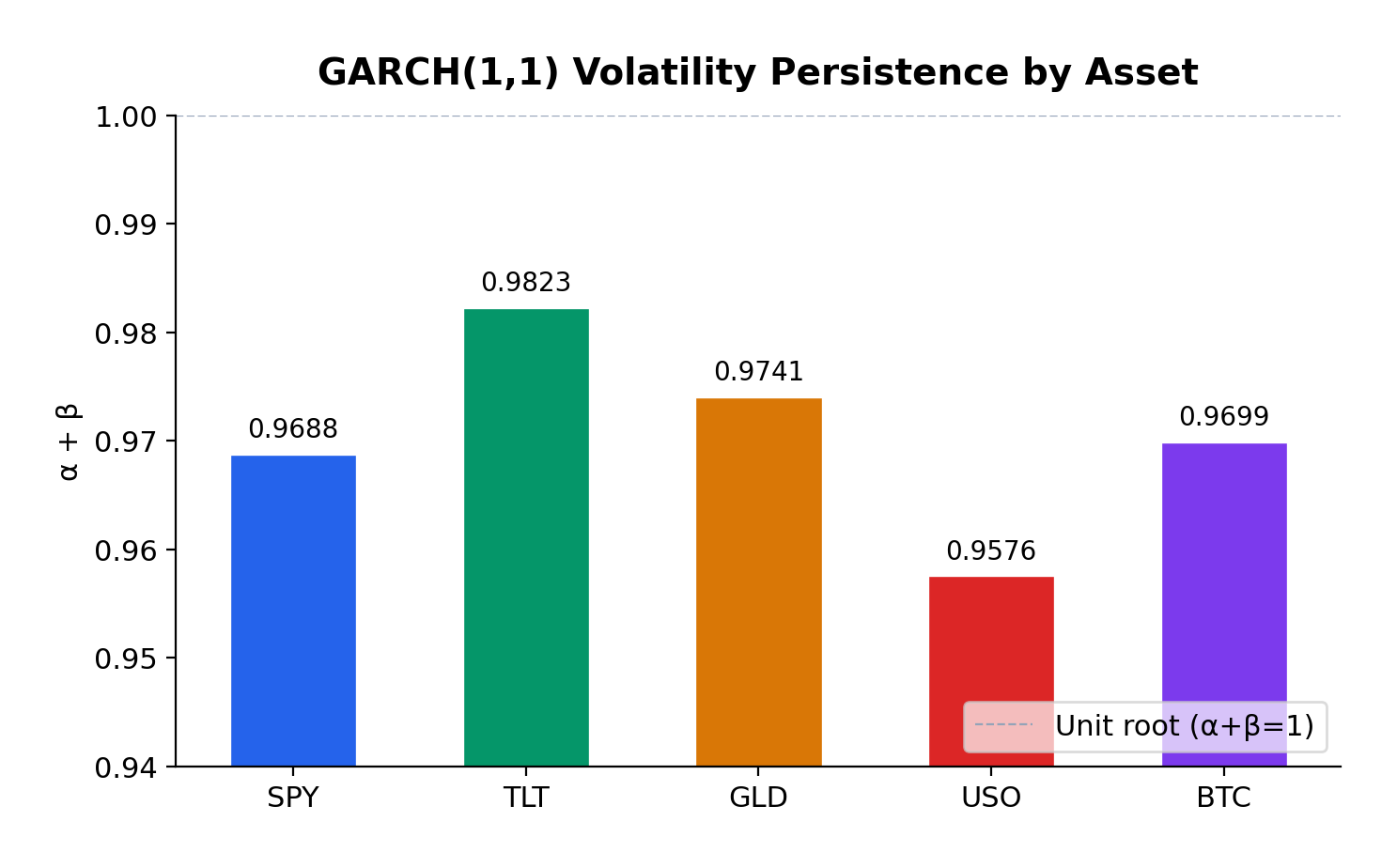

GARCH(1,1) Estimates

The GARCH(1,1) model reveals substantial variation in volatility dynamics across asset classes:

Asset

α (alpha)

β (beta)

Persistence (α+β)

Half-life (days)

AIC

S&P 500

0.1810

0.7878

0.9688

~23

7130.4

US Treasuries

0.0683

0.9140

0.9823

~38

7062.7

Gold

0.0631

0.9110

0.9741

~27

7171.9

Oil

0.1271

0.8305

0.9576

~16

11999.4

Bitcoin

0.1228

0.8470

0.9699

~24

20789.6

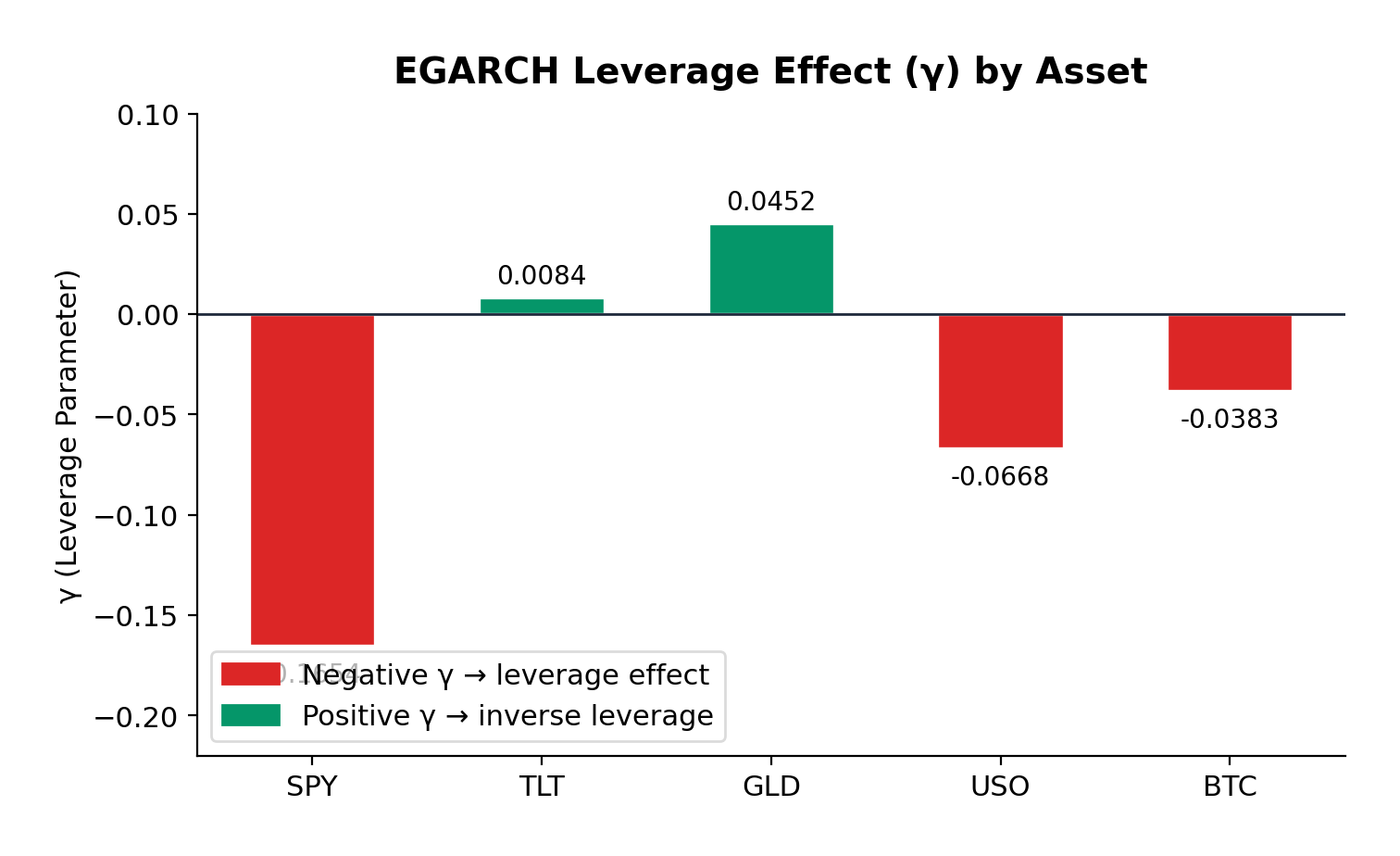

EGARCH(1,1,1) Estimates

The EGARCH model additionally captures leverage effects:

Asset

α (alpha)

β (beta)

γ (gamma)

Persistence

AIC

S&P 500

0.2398

0.9484

-0.1654

1.1882

7022.6

US Treasuries

0.1501

0.9806

0.0084

1.1307

7063.5

Gold

0.1205

0.9721

0.0452

1.0926

7146.9

Oil

0.2171

0.9564

-0.0668

1.1735

12002.8

Bitcoin

0.2505

0.9377

-0.0383

1.1882

20773.9

Volatility Persistence

All five assets exhibit high volatility persistence, with α + β ranging from 0.9576 (Oil) to 0.9823 (US Treasuries). These values are remarkably consistent with the classic empirical findings from Engle (1982) and Bollerslev (1986), who first documented this phenomenon in inflation and stock market data respectively.

US Treasuries show the highest persistence (0.9823), meaning volatility shocks in the bond market take longer to decay—approximately 38 days to half-life. This makes intuitive sense: Federal Reserve policy changes, which are the primary drivers of Treasury volatility, tend to have lasting effects that persist through subsequent meetings and economic data releases.

Gold exhibits the second-highest persistence (0.9741), consistent with its role as a long-term store of value. Macroeconomic uncertainties—geopolitical tensions, currency debasement fears, inflation scares—don’t resolve quickly, and neither does the associated volatility.

S&P 500 and Bitcoin show similar persistence (~0.97), with half-lives of approximately 23-24 days. This suggests that equity market volatility shocks, despite their reputation for sudden spikes, actually decay at a moderate pace.

Oil has the lowest persistence (0.9576), which makes sense given the more mean-reverting nature of commodity prices. Oil markets can experience rapid shifts in sentiment based on supply disruptions or demand changes, but these shocks tend to resolve more quickly than in financial assets.

Leverage Effects

The EGARCH γ parameter reveals asymmetric volatility responses—the leverage effect that Nelson (1991) formalized:

S&P 500 (γ = -0.1654): The strongest negative leverage effect in the sample. A 1% drop in equities increases volatility significantly more than a 1% rise. This is the classic equity pattern: bad news is “stickier” than good news. For options traders, this means that protective puts are more expensive than equivalent out-of-the-money calls during volatile periods—a direct consequence of this asymmetry.

Bitcoin (γ = -0.0383): Moderate negative leverage, weaker than equities but still significant. The cryptocurrency market shows asymmetric reactions to price movements, with downside moves generating more volatility than upside moves. This is somewhat surprising given Bitcoin’s retail-dominated nature, but consistent with the hypothesis that large institutional players are increasingly active in crypto markets.

Oil (γ = -0.0668): Moderate negative leverage, similar to Bitcoin. The energy market’s reaction to geopolitical events (which tend to be negative supply shocks) contributes to this asymmetry.

Gold (γ = +0.0452): Here’s where it gets interesting. Gold exhibits a slight positive gamma—the opposite of the equity pattern. Positive returns slightly increase volatility more than negative returns. This is consistent with gold’s safe-haven role: when risk assets sell off and investors flee to gold, the resulting price spike in gold can be accompanied by increased trading activity and volatility. Conversely, gradual gold price increases during calm markets occur with declining volatility.

US Treasuries (γ = +0.0084): Essentially symmetric. Treasury volatility doesn’t distinguish between positive and negative returns—which makes sense, since Treasuries are priced primarily on interest rate expectations rather than “good” or “bad” news in the equity sense.

Model Fit

The AIC (Akaike Information Criterion) comparison shows that EGARCH provides a materially better fit for the S&P 500 (7022.6 vs 7130.4) and Bitcoin (20773.9 vs 20789.6), where significant leverage effects are present. For Gold and Treasuries, GARCH performs comparably or slightly better, consistent with the absence of significant leverage asymmetry.

1. Volatility Forecasting and Position Sizing

The high persistence values across all assets have direct implications for position sizing during volatile regimes. If you’re trading options or managing a portfolio, the GARCH framework tells you that elevated volatility will likely persist for weeks, not days. This suggests:

Don’t reduce risk too quickly after a volatility spike. The half-life analysis shows that it takes 2-4 weeks for half of a volatility shock to dissipate. Cutting exposure immediately after a correction means you’re selling low vol into the spike.

Expect re-leveraging opportunities. Once vol peaks and begins decaying, there’s a window of several weeks where volatility is still elevated but declining—potentially favorable for selling vol (e.g., writing covered calls or selling volatility swaps).

2. Options Pricing

The leverage effects have material implications for option pricing:

Equity options (S&P 500) should price in significant skew—put options are relatively more expensive than calls. If you’re buying protection (e.g., buying SPY puts for portfolio hedge), you’re paying a premium for this asymmetry.

Bitcoin options show similar but weaker asymmetry. The market is still relatively young, and the vol surface may not fully price in the leverage effect—potentially an edge for sophisticated options traders.

Gold options exhibit the opposite pattern. Call options may be relatively cheaper than puts, reflecting gold’s tendency to experience vol spikes on rallies (as opposed to selloffs).

3. Portfolio Construction

For multi-asset portfolios, the differing persistence and leverage characteristics suggest tactical allocation shifts:

During risk-on regimes: Low persistence in oil suggests faster mean reversion—commodity exposure might be appropriate for shorter time horizons.

During risk-off regimes: High persistence in Treasuries means bond market volatility decays slowly. Duration hedges need to account for this extended volatility window.

Diversification benefits: The low correlation between equity and Treasury volatility dynamics supports the case for mixed-asset portfolios—but the high persistence in both suggests that when one asset class enters a high-vol regime, it likely persists for weeks.

4. Trading Volatility Directly

For traders who express views on volatility itself (VIX futures, variance swaps, volatility ETFs):

The persistence framework suggests that VIX spikes should be traded as mean-reverting (which they are), but with the expectation that complete normalization takes 30-60 days.

The leverage effect in equities means that vol strategies should be positioned for asymmetric payoffs—long vol positions benefit more from downside moves than equivalent upside moves.

At the bottom of the post is the complete Python code used to generate these results. The code uses yfinance for data download and the arch package for model estimation. It’s designed to be easily extensible—you can add additional assets, change the date range, or experiment with different GARCH variants (GARCH-M, TGARCH, GJR-GARCH) to capture different aspects of the volatility dynamics.

This analysis confirms that volatility clustering is a universal phenomenon across asset classes, but the specific characteristics vary meaningfully:

Volatility persistence is universally high (α + β ≈ 0.95–0.98), meaning volatility shocks take weeks to months to decay. This has important implications for position sizing and risk management.

Leverage effects vary dramatically across asset classes. Equities show strong negative leverage (bad news increases vol more than good news), while gold shows slight positive leverage (opposite pattern), and Treasuries show no meaningful asymmetry.

The half-life of volatility shocks ranges from approximately 16 days (oil) to 38 days (Treasuries), providing a quantitative guide for expected duration of volatile regimes.

These findings extend naturally to my ongoing work on volatility derivatives and correlation trading. Understanding the persistence and asymmetry of volatility is essential for pricing VIX options, variance swaps, and other vol-sensitive products—as well as for managing the tail risk that inevitably accompanies high-volatility regimes like the one we’re navigating in early 2026.

References

Engle, R.F. (1982). “Autoregressive Conditional Heteroskedasticity with Estimates of the Variance of United Kingdom Inflation.” Econometrica, 50(4), 987-1007.

Bollerslev, T. (1986). “Generalized Autoregressive Conditional Heteroskedasticity.” Journal of Econometrics, 31(3), 307-327.

Nelson, D.B. (1991). “Conditional Heteroskedasticity in Asset Returns: A New Approach.” Econometrica, 59(2), 347-370.

All models estimated using Python’s arch package with normal innovations. Data source: Yahoo Finance. The analysis covers the period January 2015 through February 2026, comprising approximately 2,800 trading days.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.