Streaming subscriptions have become one of those expenses that quietly chip away at your budget month after month. That’s why it’s worth paying attention when a credit card includes one at no additional cost.

Through Dec. 31, the Chase Sapphire Preferred® Card (see rates and fees) comes with a complimentary one-year Apple TV subscription — a lesser-known perk that can easily offset the card’s annual fee for eligible cardholders.

If you’re paying for the streaming service (or have been meaning to try it out), activating the benefit can save you the cost of a full year of access to Apple’s growing catalog of original shows and movies.

Here’s what you need to know about this benefit and how to activate it.

Limited-time offer on the Chase Sapphire Preferred: Earn 100,000 bonus points after spending $5,000 on purchases in the first three months from account opening.

What is the Chase Sapphire Preferred Apple TV benefit?

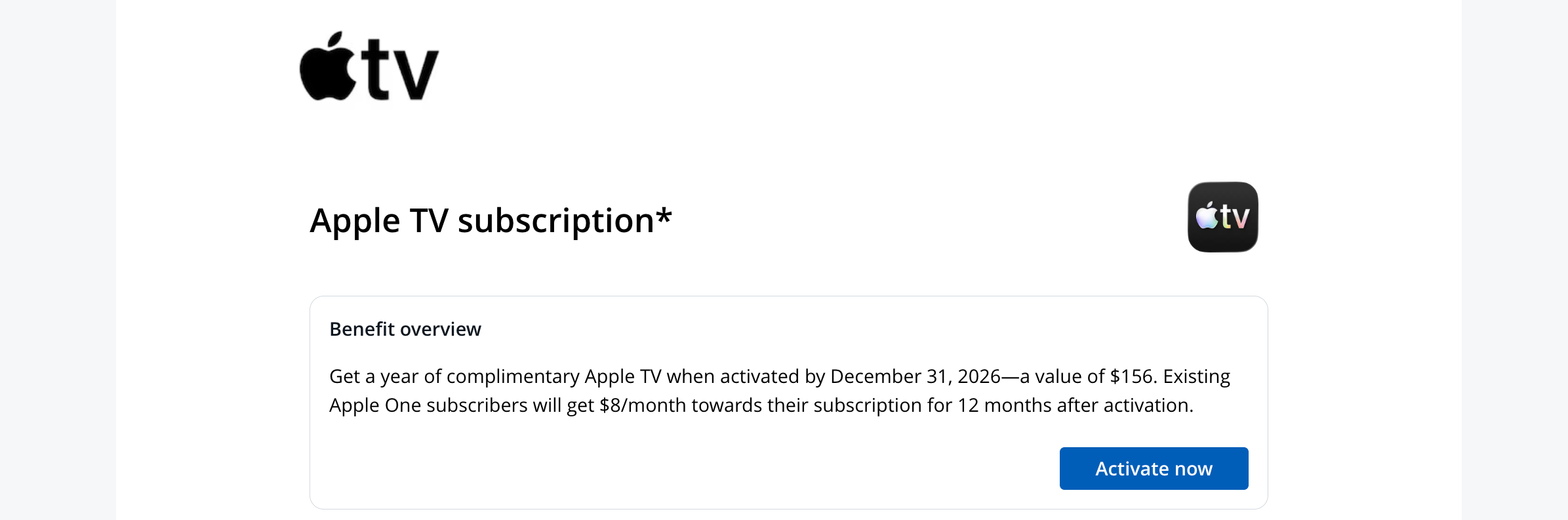

Chase Sapphire Preferred Card holders are eligible for a complimentary Apple TV subscription for one year (when they activate the benefit by Dec. 31).

Unlike a statement credit, this benefit provides direct access to the service, so you don’t need to pay for a subscription and wait for reimbursement. Once activated, you’ll receive one year of Apple TV at no cost.

Apple TV gives subscribers access to original programming, including popular shows such as “Ted Lasso,” “Severance” and “The Morning Show,” as well as a growing library of movies, documentaries and family content.

To take advantage of the offer, you must activate the benefit through Chase and link an Apple ID.

Reward your inbox with the TPG Daily newsletter

Join over 700,000 readers for breaking news, in-depth guides and exclusive deals from TPG’s experts

Related: Chase Sapphire Preferred statement credits: What they are and how to use them

How to activate your complimentary Apple TV subscription

Activating your Apple TV subscription is straightforward and can be completed through either Chase’s website or mobile app.

Start by logging in to your Chase account and navigating to the “Benefits” section associated with your Sapphire Preferred Card. From there, locate the Apple TV benefit and select “Activate Now.”

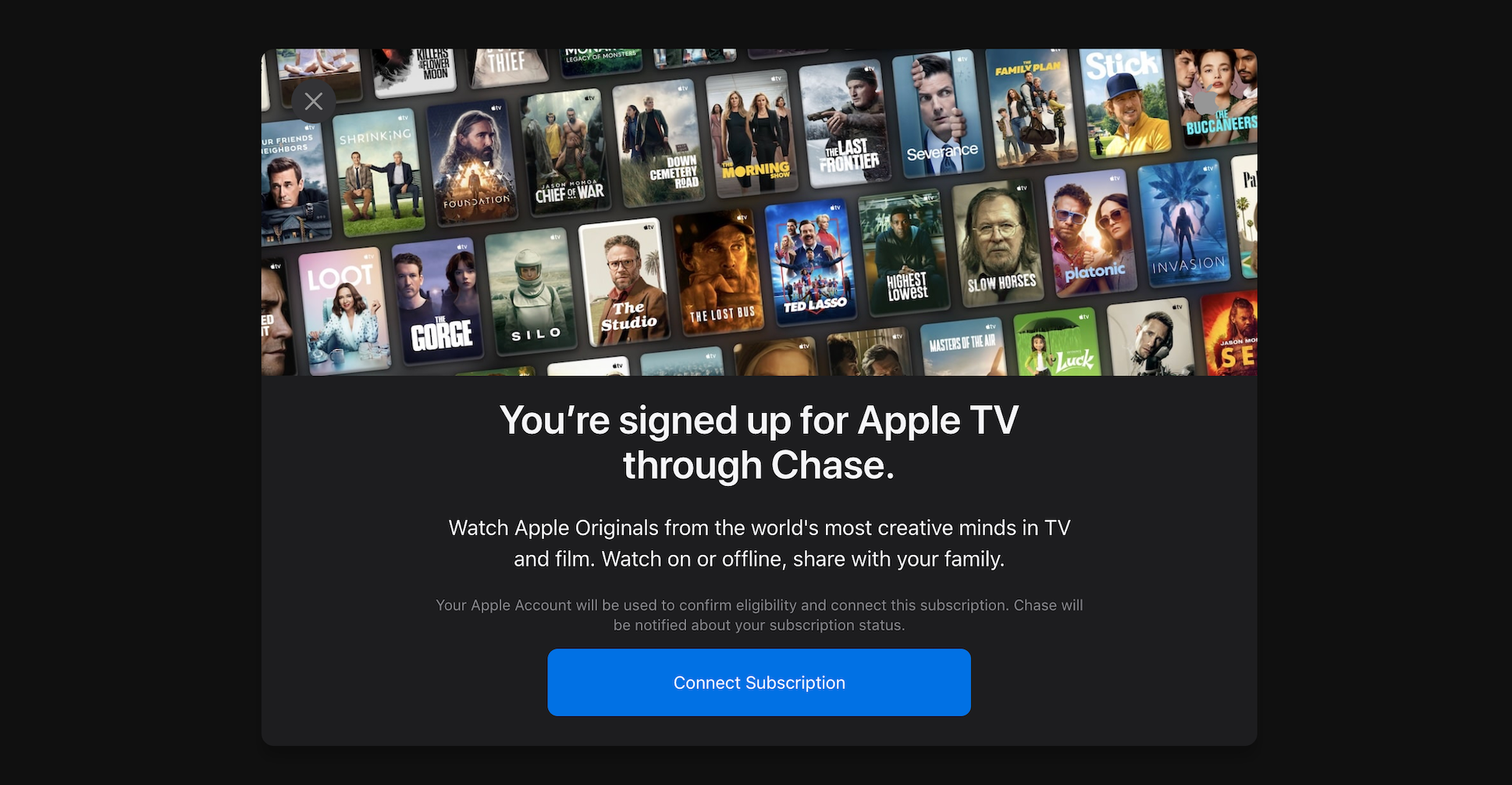

You’ll then be directed to Apple TV, where you’ll be prompted to sign in with (or link) your Apple ID. Once connected, your complimentary one-year subscription will be activated.

If you currently pay for Apple TV directly through Apple, activating the Chase benefit will pause your existing subscription. Once the complimentary subscription ends, your paid Apple TV subscription will automatically resume at the then-current rate.

Related: 8 Chase Sapphire Preferred benefits you might not know about

Is the Apple TV benefit worth it?

Apple TV currently costs $12.99 per month or $99.99 annually. That means a one-year complimentary subscription is worth at least $100 (and as much as $156 before taxes if you would otherwise pay month-to-month for a full year).

Either way, the benefit more than offsets the Chase Sapphire Preferred’s $95 annual fee on its own.

Of course, the value of any credit card perk depends on whether you’d otherwise use it. If Apple TV isn’t currently part of your entertainment budget, this benefit may not deliver its full advertised value. However, it does offer a risk-free opportunity to explore the platform’s content library for a year.

Beyond the complimentary subscription, Sapphire Preferred Card holders can also earn 3 points per dollar spent on eligible streaming service purchases, including Apple Music, Apple TV, Disney+, Hulu, Netflix, Spotify and YouTube Premium.

Keep in mind that this benefit only covers Apple TV and does not include Apple Music. Cardholders seeking a wider range of Apple-related perks may get more value from the Chase Sapphire Reserve® (see rates and fees).

Related: 1 Chase Sapphire Preferred perk now offsets its $95 annual fee

Bottom line

The Chase Sapphire Preferred includes a complimentary one-year Apple TV subscription for cardholders (who activate the benefit by Dec. 31).

Since Apple TV costs $99.99 annually, this perk can more than offset the card’s $95 annual fee for cardholders who would otherwise pay for the service.

If you’re a Sapphire Preferred Card holder, activating the benefit takes just a few minutes and can provide a full year of access to Apple’s growing catalog of original shows and movies.

To learn more, read our full review of the Chase Sapphire Preferred.

Apply here: Chase Sapphire Preferred Card

Stacie Harris is a local resident and reporter of the Maple Grove area. Stacie reports on medicine and science for the Maple Grove Report.