One of the best ways to redeem Ultimate Rewards points is via high-value Chase transfer partners. But Chase recently announced it was reducing the Chase-to-Hyatt transfer ratio for select cardholders. Unfortunately, the Chase Sapphire Preferred® Card (see rates and fees) is among the affected cards.

As a Sapphire Preferred Card holder, I’m bummed about the reduced Hyatt transfer ratio and wanted to quantify the impact of this change.

Here’s what you should know about the reduced transfer ratio and how it will affect the amount you need to spend on your card to earn the same Hyatt stays.

Chase Sapphire Preferred Card: For a limited time, earn 100,000 bonus points after spending $5,000 on purchases in the first three months from account opening.

New Chase-to-Hyatt transfer ratio

If you applied for the Chase Sapphire Preferred Card on or after June 15, you’ll already have the reduced 4:3 transfer rate if you transfer Chase points to Hyatt.

But if you applied before June 15, you’ll continue to get a 1:1 transfer rate until Oct. 1, when your Chase-to-Hyatt transfer ratio will also drop to 4:3.

Why this matters for Sapphire Preferred Card holders

A reduced transfer ratio between Chase Ultimate Rewards and World of Hyatt makes Hyatt awards more expensive for Sapphire Preferred Card holders.

For example, whereas at a 1:1 transfer ratio you’d only need to transfer 30,000 Chase points to book a 30,000-point Hyatt award, at a 4:3 transfer ratio you’d need to transfer 40,000 Chase points to book the same award.

Based on TPG’s June 2026 valuations, these additional 10,000 Chase points you’d need to transfer are worth $205.

Reward your inbox with the TPG Daily newsletter

Join over 700,000 readers for breaking news, in-depth guides and exclusive deals from TPG’s experts

Examples of how many more Chase points you’ll need

To illustrate the impact of the reduced 4:3 transfer ratio for Chase-to-Hyatt transfers, let’s consider three stays.

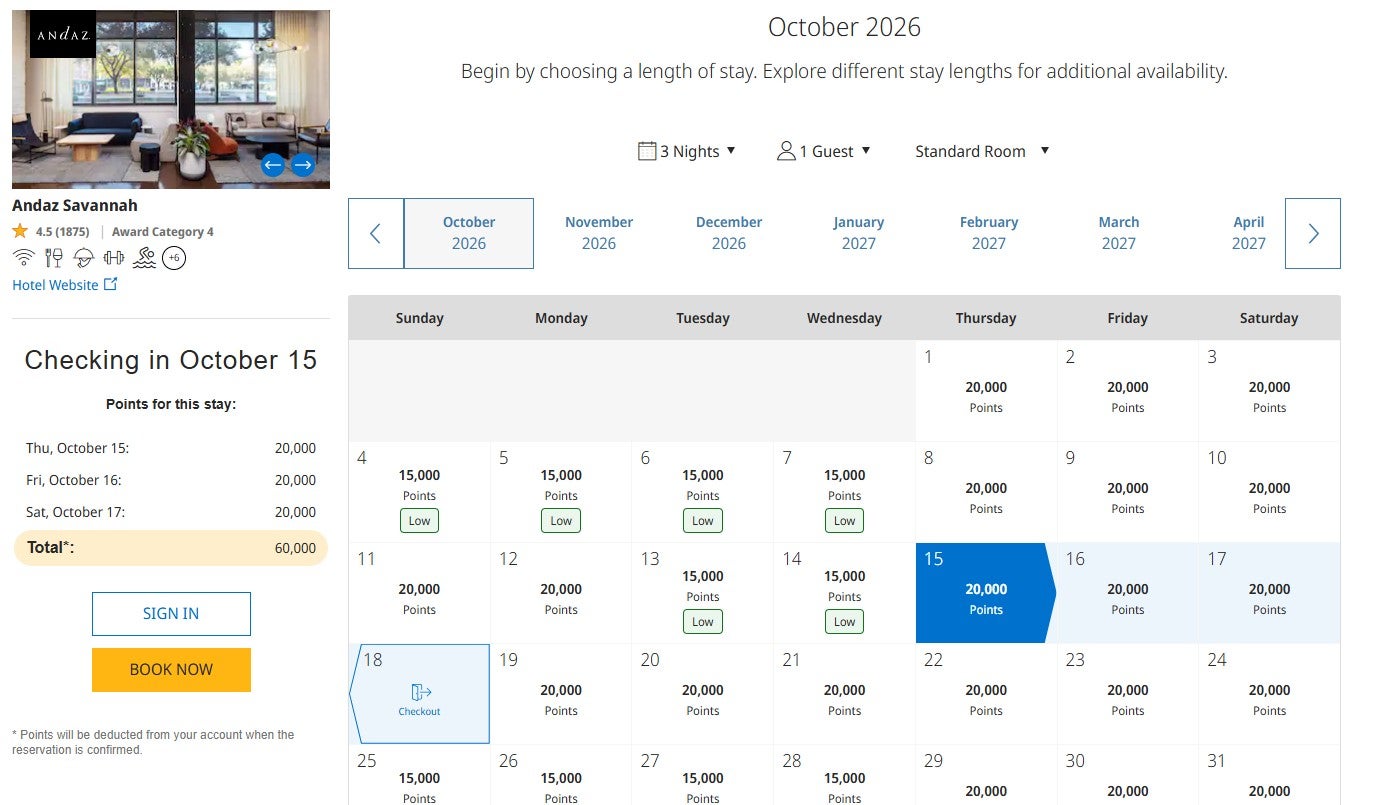

Firstly, let’s consider a long-weekend stay at the Andaz Savannah that costs 20,000 points per night. With a 1:1 transfer ratio, you’d only need to transfer 60,000 Chase points. But under a 4:3 transfer ratio, you’d need to transfer 80,000 Chase points. The extra 20,000 points you’d need to transfer are worth $410 based on our valuations.

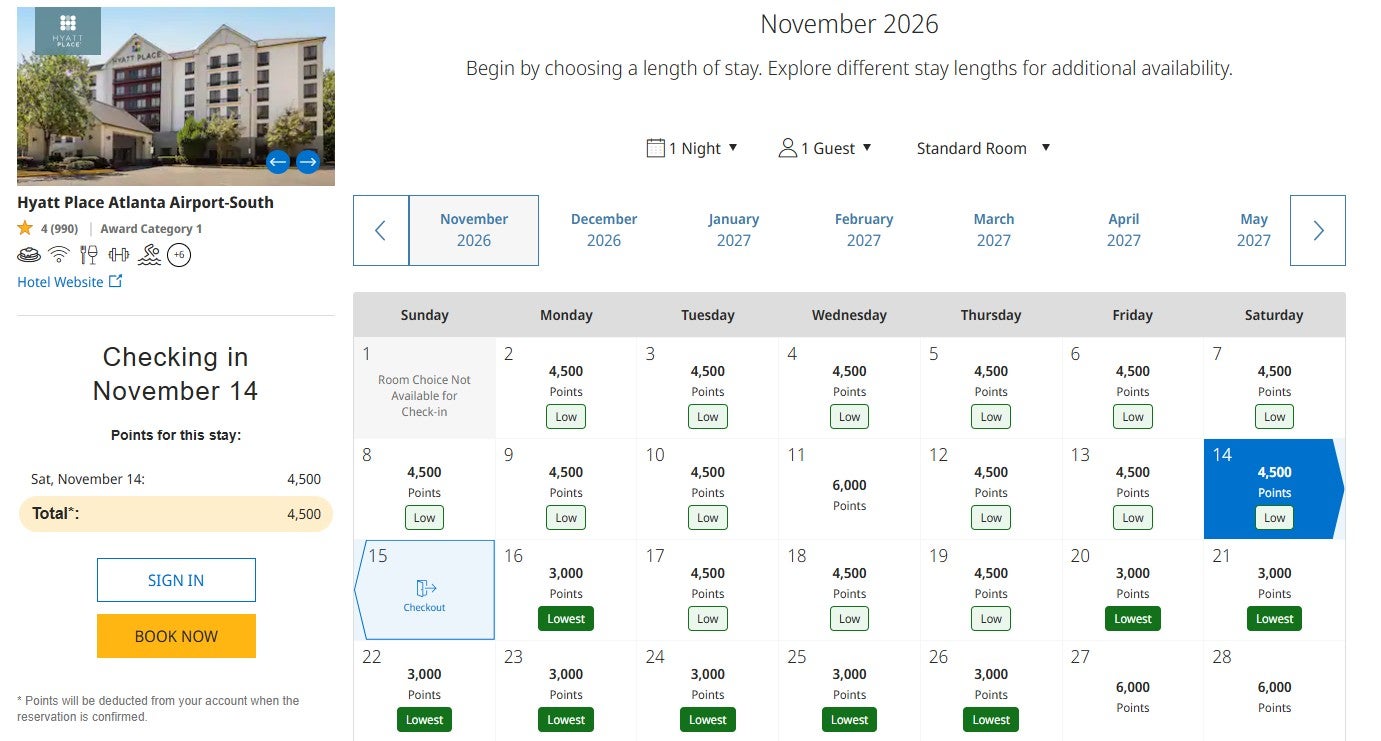

Now, let’s consider a redemption I book several times each year: a one-night stay at a Hyatt Place in Atlanta (with complimentary airport shuttle service).

If this hotel costs 4,500 Hyatt points on the night I need to stay, I’d need to transfer 5,000 Chase points at a 1:1 ratio or 6,000 Chase points at a 4:3 ratio (since you must transfer in increments of 1,000 points). So, even for a one-night stay at a Category 1 Hyatt hotel, this decreased transfer ratio makes a difference.

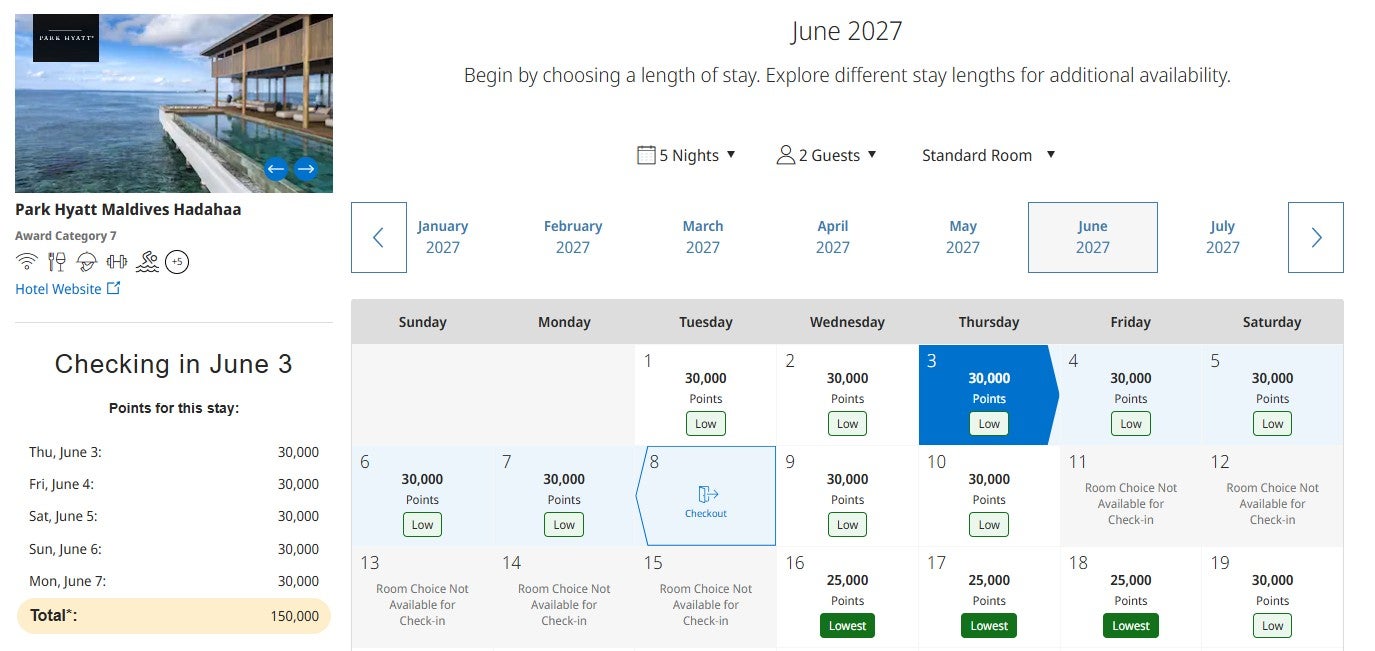

Finally, let’s consider a five-night stay at an aspirational Category 7 Hyatt that costs 30,000 points per night. With a 1:1 transfer ratio, you’d need to transfer 150,000 Chase points to Hyatt to book this stay.

But, with a 4:3 transfer ratio, you’d need to transfer 200,000 Chase points. The extra 50,000 Chase points you’d need to transfer under a 4:3 transfer ratio instead of a 1:1 transfer ratio are worth $1,025 based on our valuations.

What does that mean in everyday spending?

Another way to think about the change is how much more you’ll need to spend to earn the same Hyatt vacation.

As a reminder, purchases with the Chase Sapphire Preferred earn as follows:

- 5 points per dollar on all Chase Travel℠ purchases, including flights, hotels, rental cars, vacation homes, cruises, activities and tours

- 5 points per dollar spent on Lyft rides (through Sept. 30, 2027)

- 5 points per dollar spent on eligible Peloton equipment and accessory purchases over $150 (through Dec. 31, 2027; limit of 25,000 bonus points)

- 3 points per dollar spent on gas and EV charging

- 3 points per dollar spent on vacation homes at these top brands: Airbnb, Vrbo, Plum Guide, HomeAway, Homestay.com and Vacasa

- 3 points per dollar spent on dining, streaming services and online groceries (the elevated earning rate for online grocery store purchases excludes Target, Walmart and wholesale clubs)

- 2 points per dollar spent on all other travel

- 1 point per dollar spent on all other purchases

Related: Is the Chase Sapphire Preferred worth the annual fee? I say yes

Each consumer is different, so you’ll need to calculate based on your own spending habits. But, to see how this plays out, let’s consider three different spending profiles:

- Single-card user: 5 points per dollar on 5% of purchases, 3 points per dollar on 20%, 2 points per dollar on 10% and 1 point per dollar on 65%

- Bonus category optimizer: 5 points per dollar on 15% of purchases, 3 points per dollar on 55% and 2 points per dollar on 30%

- 3-points-per-dollar-or-better user: 5 points per dollar on 30% of purchases and 3 points per dollar on 70%

| Spending required | By the single-card user | By the bonus category optimizer | By the 3-points-per-dollar-or-better user |

|---|---|---|---|

|

For a 4,500-point Hyatt stay

|

|

|

|

|

For a 60,000-point Hyatt stay

|

|

|

|

|

For a 150,000-point Hyatt stay

|

|

|

|

As you can see, the difference between a 1:1 Chase to Hyatt transfer ratio and a 4:3 ratio is huge when it comes to the amount you’ll need to spend on your Chase Sapphire Preferred for a stay.

Should Sapphire Preferred Card holders still transfer points to Hyatt?

The reduced Chase-to-Hyatt transfer ratio makes it much less appealing for Sapphire Preferred Card holders to transfer Chase points to Hyatt.

While it may still be valuable to transfer Chase points to Hyatt at a 4:3 ratio to top off your Hyatt account for a redemption or snag a high-value Hyatt redemption, Sapphire Preferred cardholders should seriously consider whether other Chase transfer partners they can still access at a 1:1 ratio provide more value.

If you applied for the Sapphire Preferred before June 15, you still have access to 1:1 Chase to Hyatt transfers through Sept. 30. But, after that point, all Sapphire Preferred cardholders will face a reduced 4:3 Chase to Hyatt transfer ratio.

As you can see in the previous sections, this reduced transfer ratio has a significant impact. As such, Sapphire Preferred cardholders may want to consider another way to earn Hyatt points.

And cardholders who are accustomed to transferring most of their rewards to Hyatt may want to add the Chase Sapphire Reserve® (see rates and fees) or the Chase Sapphire Reserve for Business℠ (see rates and fees) to their wallet. You can combine your points earned on the Sapphire Preferred with these two cards and transfer them to Hyatt at a 1:1 ratio.

Bottom line

The drop from a 1:1 to 4:3 Chase-to-Hyatt transfer ratio is a meaningful devaluation for Chase Sapphire Preferred Card holders who frequently transfer Ultimate Rewards points to World of Hyatt.

Put simply, you’ll need one-third more Chase points — and therefore significantly more card spending — to book the same Hyatt awards with a 4:3 ratio instead of a 1:1 ratio.

Hyatt is still a worthwhile Chase transfer partner in some cases, especially if you only need to top off your account or find an especially high-value award. But Sapphire Preferred Card holders should run the numbers more carefully going forward and consider whether another Chase transfer partner, a Hyatt credit card or a Sapphire Reserve product offers better value.

Related: Chase Sapphire Preferred vs. Sapphire Reserve: Which is better for you?

Stacie Harris is a local resident and reporter of the Maple Grove area. Stacie reports on medicine and science for the Maple Grove Report.